Types of Long Term Incentive Plans

|

By: Mansour Baker

|

Posted: 01 November 2019

|

Revised: 23 April 2020

|

|

By: Mansour Baker

|

Posted: 01 November 2019

|

Revised: 23 April 2020

|

|

Long term incentive plans (LTIP) are to drive short-term, mid-term and long-term performance to motivate, enhance performance and retain employees.

Long-term Incentive Plans Objectives

Create Shareholder Value

Encourage Employee Performance

Retention

Ease of Implementation

Align with Market Practice

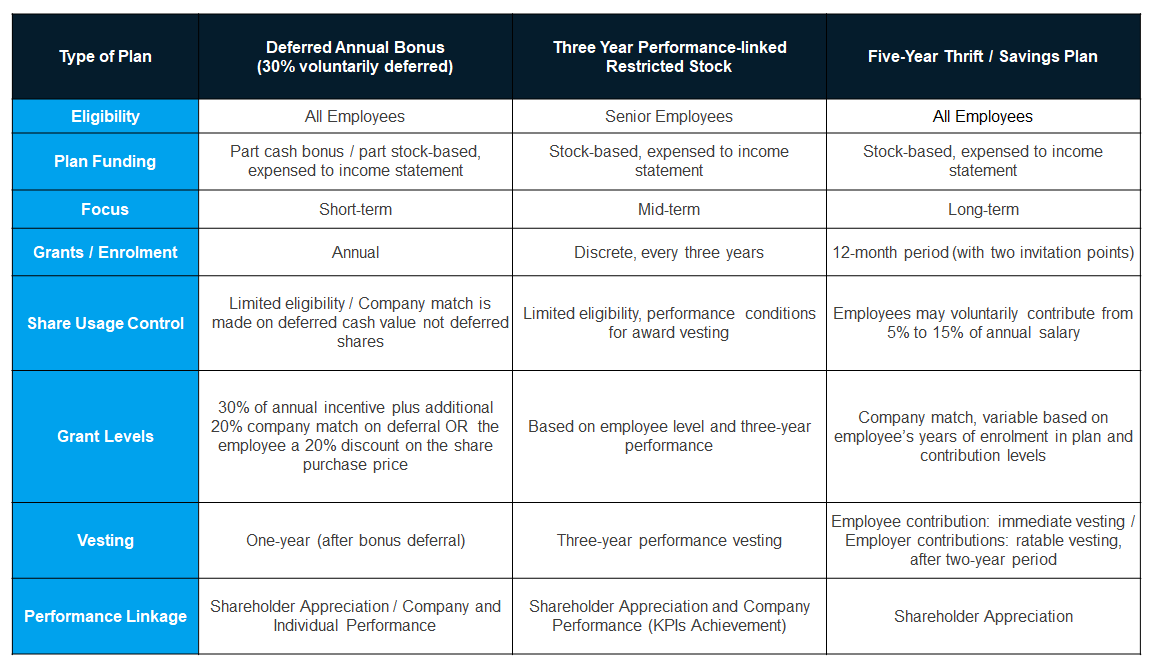

Exhibit 1

Summary of Long Term Incentive Plans

The three plans would help drive short-term, mid-term and long-term performance

|

|

Three Types of Long Term Incentive Plans

1. Deferred Restricted Stock Annual Bonus

Plan would encourage employee retention, drive short term performance and mitigate risk.

2. Three Year Performance Restricted Stock

Plan ties performance requirements to restricted stock allocations, driving performance over the three-year vesting period.

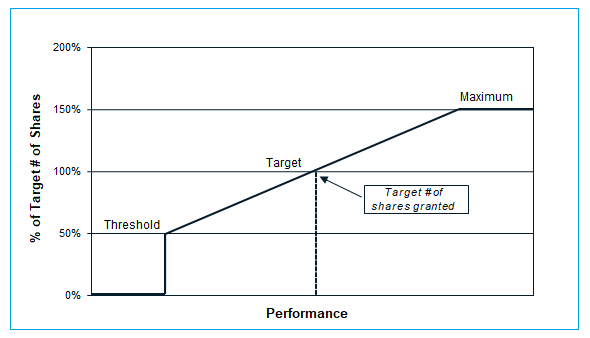

Exhibit 2

Target and Maximum Award Values

|

|

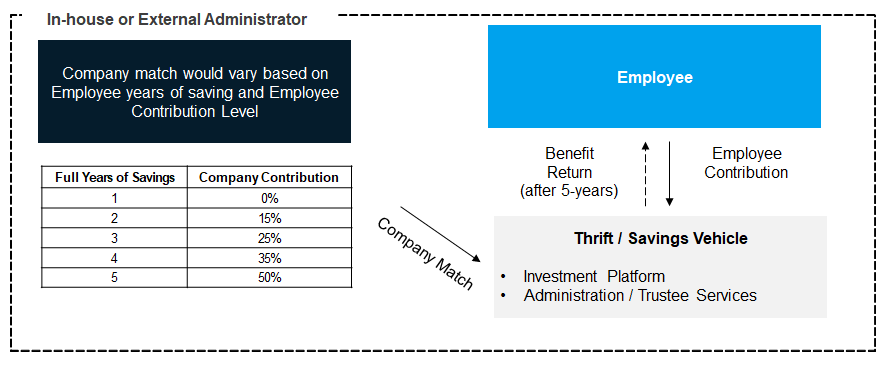

3. Five Year Thrift / Savings Plan

An integrated incentive and savings scheme for all company employees to buy shares.

Exhibit 3

Saving Plan Model

|

|

Leavers

Leaver provisions provide a basis for dealing with (good leavers and bad leavers) participants leave the organization prior to the vesting period. Good Leavers

Bad Leavers

Implementation Steps

|